Every real estate investor must understand how 1031 exchanges work. Not knowing will cost you lots of money.

Every real estate investor must understand how 1031 exchanges work. Not knowing will cost you lots of money.

What is a 1031 Exchange?

IRS 1031 Exchanges originated with the Revenue Act of 1921.

Internal Revenue Code Section 1031 lets taxpayers sell any type of real estate investment, income, or business property and use the sales proceeds to buy other types of similar properties.

The IRS lets you defer paying capital gains taxes. Likewise, most states with an income tax follow the federal government and defer their state taxes too. Let’s explore the requirements.

1031 Like-Kind Exchanges Requirements

Like any tax law, the 1031 exchange law has several requirements to qualify.

Only Exchange Qualified Like-Kind Properties

The IRS calls the process of selling business, income, and investment real properties and buying other similar properties as “Like-Kind Exchanges”. That’s because exchanging real property used as investments, income, or for business is considered the same. Confused?

Let’s clear this up. Section 1031 of the Internal Revenue Code defines “Like Kind” as real estate used for investment, income, or business purposes.

The IRS offers these examples:

- Selling an apartment building to buy another apartment building;

- Sell an apartment building to buy investment raw land;

- Sell raw land held for investment purposes and buy an office building; and

- Selling an office building to buy several multi-family homes to rent.

In other words, sell any type of business, income, or investment property and use the funds to buy more investment, income, or business properties.

Non-Qualified Properties: As mentioned above, only real properties used for business, income, or investment purposes qualify. Buying property for a quick resale (“fix and flip”) does not qualify. Similarly, a personal residence doesn’t qualify.

Equal or Greater Value, Equity, and Debt

When you sell your business or investment real estate you must buy one or more similar properties totaling equal or greater in value, equity, and debt.

The formula established by the 1031 law calls for:

- Holding a business or investment property for at least “one year and a day” before exchanging;

- The total of the exchanged (replacement) properties must equal or be greater than the value of the sold property;

- The equity in the replacement properties must equal or be greater than the sold property; and

- The debt of the replacement properties must equal or be greater than the sold property.

Seems confusing? Here is an example of how the IRS formula works.

If you sell a rental home for $200,000 with a mortgage of $50,000 and equity of $150,000 you must:

- Buy a rental house or other properties totaling $200,000 or more;

- Carrying at least a loan of $50,000; and

- The total equity of $150,000 must be equal to or greater.

Have questions?

Timing Requirements to Identify and Buy the Replacement Properties

The 1031 law sets up timing deadlines to complete the exchange.

- A 1031 exchange requires identifying candidates for the replacement properties within 45 days of the sale’s closing date; and

- Finish all purchases within 180 days of the sale’s closing date.

45-Day Rule: The 45-day requirement means preparing a list of potential replacement properties using addresses or legal descriptions. You must sign and date the list and send it to your intermediary who keeps it in case the IRS asks for it.

Tip: Either have a witness sign and date the list or sign it before a notary public who stamps a seal on it.

180-Day Rule: The official closing date on all purchases verifies the 180-day rule was met.

1031 Qualified Intermediary Required

The 1031 exchange law requires a “Qualified Intermediary” to hold and control the sales proceeds in “trust” to use as payment for the replacement properties. The IRS requires your funds must be held in a “Safe Harbor” by a qualified intermediary.

Only a neutral third-party qualifies as an intermediary. Your attorney, stock broker, accountant, or Realtor do not qualify. Likewise, your employees, family, other relatives, and friends don’t qualify.

Basically, the IRS doesn’t trust you to hold on to the sales proceeds. You must prove the same funds from the sale bought the replacement properties.

Thus, an entire industry grew from the 1031 law known as “1031 Intermediaries” or “1031 Facilitators” to handle the funds in a special escrow account. They are inexpensive and available nationwide. Our Big Block Realtors will know some to recommend.

As long as the sales proceeds never come into possession or control of the taxpayer the 1031 exchanges become totally tax-deferred when done correctly.

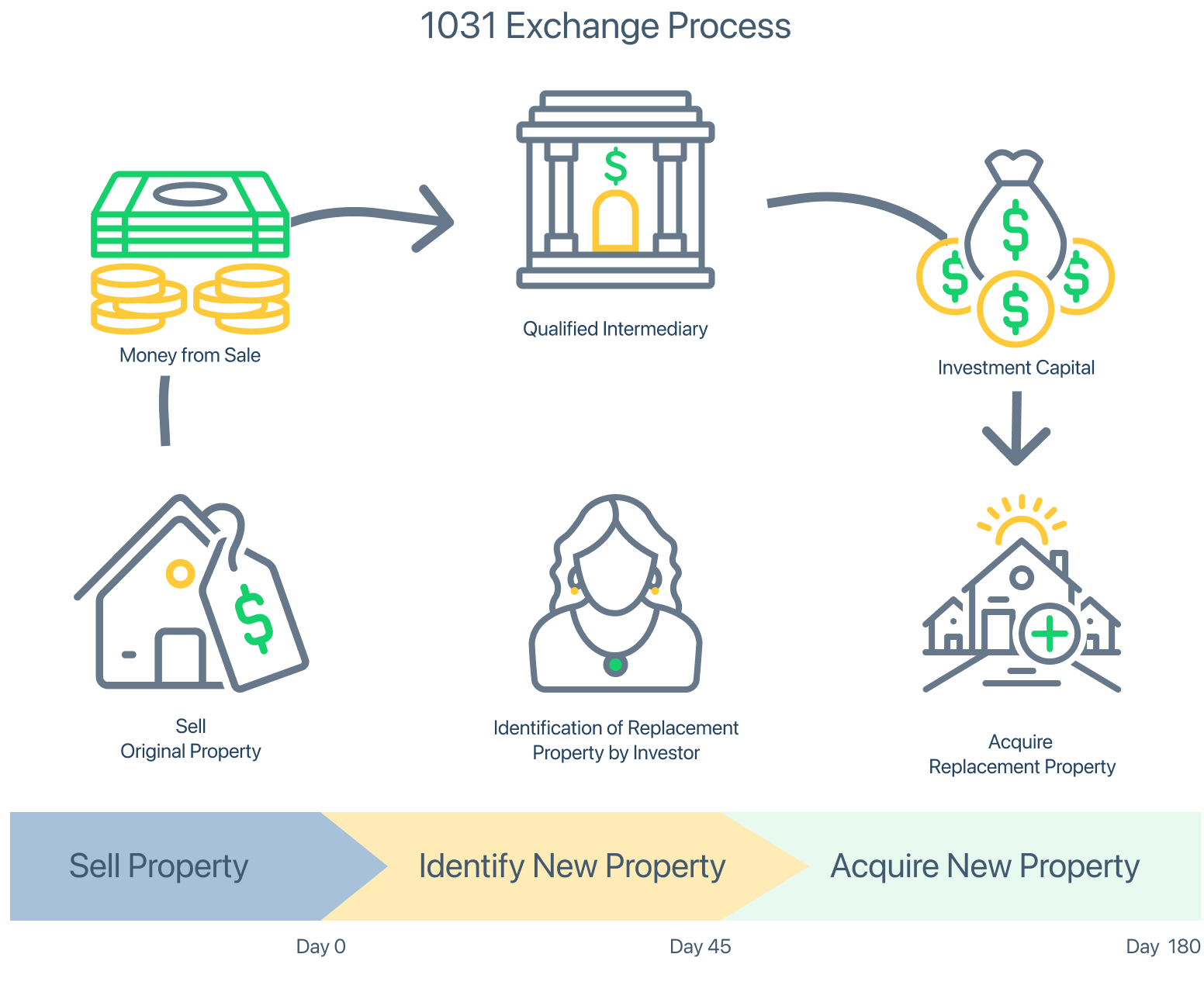

How the 1031 Exchange Process Works

Source Licensed for Commercial Use by Spruce

What Types of Properties Qualify for 1031 Exchanges?

All types of business properties qualify for a 1031 Like-Kind Exchange. Examples include:

- Apartment buildings;

- Single and multifamily rentals;

- Hotels and motels;

- Gas stations;

- Shops;

- Grocery or retail stores;

- Shopping malls; and

- Warehouses.

Properties held for investment or income purposes include:

- Raw land;

- Condo units and houses rented out; and

- Commercial and industrial buildings held for profit or leased.

Mix and Match: You are not limited to only buying business properties if you sell a business. The IRS lets you sell any type of business property to buy investment or income properties and vice versa.

Keep Exchanging and Never Pay Taxes

The beauty of 1031 Like-Kind Exchanges is to keep exchanging until you either sell or pass away.

When you sell, the deferred taxes become due. Depending on future tax law changes you may find a time to sell to pay little or no taxes (if the government abolishes them or lowers the tax rate).

If you hold on to the properties until you pass away the law forgives the deferred taxes when they pass onto your heirs. Tax experts call this a “step-up in basis” where your heirs take ownership owing no federal taxes.

A step-up in basis occurs when the government adjusts the value (“cost basis”) of inherited assets (like real estate). For instance, the capital gains tax is eliminated due to the heirs receiving the assets as a “step-up” to its current fair market value.

For example, a rental home sold at a $200,000 fair market price and exchanged for business or investment properties. Over the years, after several exchanges, the fair market value equals $2 million. If sold, the increase of value by $1.8 million becomes subject to the capital gains tax. Yet, if the owner dies and the properties are inherited the increased value carries over to the heirs. If your heirs sell the properties for $2 million no federal taxes are paid.

Round and Round it Goes: Look at 1031 exchanges as a fun merry-go-round increasing in value over the years. When the original owner dies the heirs get rewarded (a brass ring) by owing no taxes. Only when the heirs hold on to the properties and sell them for a higher value will they owe taxes. Unless they decide to do a 1031 Like-Kind Exchange. The merry-go-round keeps turning.

Bonus: Your heirs avoid paying the federal Estate Tax due to the stepped-up basis.

Reporting Like-Kind Exchanges to the IRS

Use Form 8824, called “Like-Kind Exchanges” to report your real estate sales and replacement purchases to the IRS.

Form 8824 includes information about this law and instructions on how to complete the form.

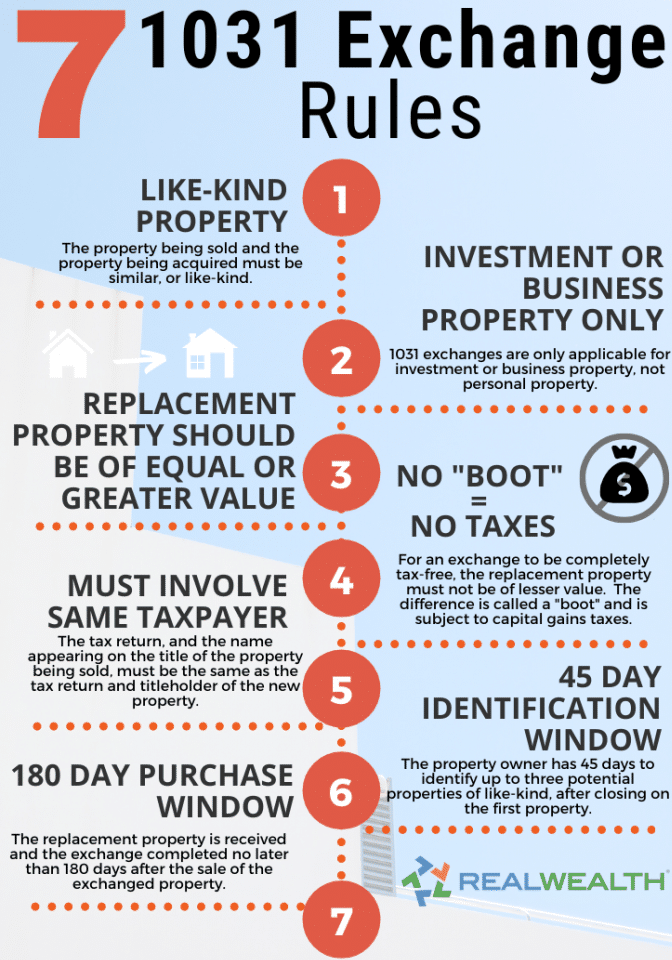

The 7 Rules for a 1031 Like-Kind Exchange

Source Licensed for Commercial Use by the RealWealth Network

How 1031 Exchanges Work – Conclusion

Now that you learned how 1031 exchanges work, let’s highlight the important features.

To summarize, a 1031 Exchange involves investment, income, or business property sold with the proceeds held by an intermediary who re-invests into other business, income, or investment properties.

Tax-Deferred: Under Internal Revenue Code Section 1031 the IRS will not recognize either a gain or a loss for tax purposes. The law defers all capital gains taxes for every exchange until the taxpayer sells or dies.

Qualified Properties: A 1031 exchange requires selling and buying qualified properties like business, income, and investment properties. Fix and flip or personal residence properties don’t qualify.

Like-Kind: Any type of business, income or investment properties exchanged for other business, income, or investment properties are “like-kind”.

Holding Period: The IRS requires holding onto qualified properties for at least a year and a day.

Equal or Greater Value: You must buy replacement properties equal or greater in value than the one(s) sold.

Equal or Greater Equity: The replacement properties must carry the same or more debt than the one(s) sold.

Exchange Required: An “exchange” occurs by using a qualified intermediary to hold the sales proceeds who uses them to buy replacement properties. The seller cannot possess or control the funds.

Timing Requirements: The 45 Day Rule requires identifying all candidates for replacement properties within 45 days from the closing date of the sale. The 180 Day Rule requires completing all purchases within 180 days of the closing.

Failure to Meet the Deadlines results in a typical sale with all capital gains taxes due.

Ending 1031 Exchanges: Two options exist,

- (1) Cash Out and pay the deferred taxes; or

- (2) Pass Away and Pass it On where your heirs enjoy a “stepped-up basis” with no deferred capital gains tax or estate tax due.

Interested in Doing a 1031 Like-Kind Exchange in San Diego County?

After reading about the many tax benefits for yourself and your heirs by doing a 1031 Exchange, do you have business, income, or investment properties to sell?

Big Block Realty provides experienced Realtors with 1031 Exchanges to guide you from listing your properties for sale through the exchange process and closing on your replacement properties.

Contact us before listing your qualified properties for sale. You need the knowledge, expertise, and guidance of our Realtors to save you from paying capital gains taxes and your heirs paying estate taxes.

Steven Rich, MBA – Guest Blogger

Search Local Real Estate Below Or Use Our: Home Search Tool:

—

HAVE ANY QUESTIONS?

Let us know, we love to help:

Call: (800) 550 – 3209

or Click: www.BigBlockRealty.com/contact

—

Connect with Big Block…

SUBSCRIBE TO OUR CHANNEL: https://www.youtube.com/@bigblockrealty?sub_confirmation=1

CONNECT WITH US ON SOCIAL HERE: https://bigblockrealty.com/social/

Find us on Instagram: https://www.instagram.com/BigBlockRealty_